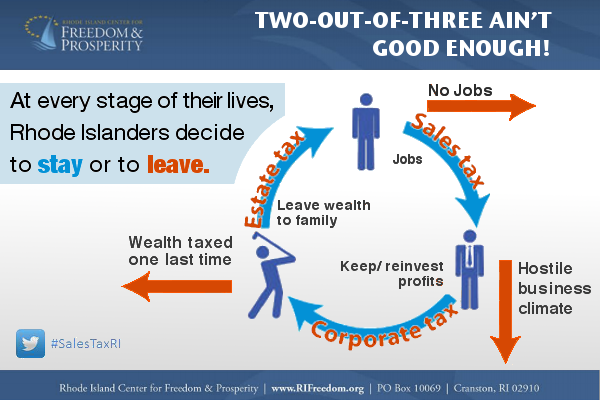

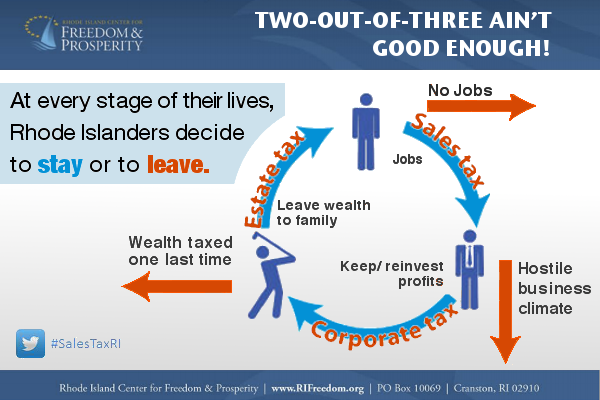

New Study: higher tax burden reduces state economic growth & population

August, 2014 – We consistently hear Rhode Island lawmakers claim that citizens or the wealthy can “afford” some minor, new tax to pay for some new government project. That may be true in some cases.

But what is also true, in almost all cases, is that OUR STATE’S ECONOMY CANNOT AFFORD THE TAX HIKES.

A new study by the nationally renowned Mercatus Center explains this cause and effect.

***

Read below or go to the Mercatus page here; http://mercatus.org/publication/state-economic-prosperity-and-taxation

State Economic Prosperity and Taxation

Policymakers frequently debate how different methods of taxation affect their states’ economies. While most economists agree that higher taxes result in reduced investment and innovation, previous studies have not found overwhelming evidence that higher tax rates lead to lower economic growth.

To untangle this paradox, new research by economist Pavel Yakovlev for the Mercatus Center at George Mason University examines the effects of taxation on states’ economic performance, businesses growth, and net migration rates. The study finds that higher state taxes correlate with lower economic performance, even when controlling for various factors. The magnitude and significance of this effect varies depending on the type of taxes and the type of economic activity in question. The study analyzes the relationship between states’ economic performance and tax variables including effective average tax rates, the personal income tax, and personal income tax progressivity.

To read the study in its entirety, please see “State Economic Prosperity and Taxation.”

KEY FINDINGS

- A higher average tax burden reduces state economic growth. Dividing total tax revenue by gross state product (GSP) shows that a 1 percent increase in a state’s average tax rate is associated with a decrease of 1.9 percent in the growth rate of its GSP.

- Taxes impact migration patterns. If higher state taxes lead to lower economic activity and employment, it is conceivable that people will move to states with better economic prospects. Of the nine states with no personal income tax, four—Florida, Nevada, Washington, and Tennessee—are among the states with the highest population growth rates in the country in recent decades. Also, data show that a higher personal income tax rate is associated with a higher probability of residents migrating to a state with a lower tax rates.

- Income tax progressivity affects the number of new firms. The number of new firms opening in a state is a key indicator of beneficial creative destruction and innovation that will improve living standards for the state’s residents over time. Other studies have found that new firm entry accounts for 20–50 percent of a state’s overall productivity growth. The latest economic data show that the rate of start-up creation is sensitive to personal income tax progressivity. A 1 percent increase in personal income tax progressivity is associated with a reduction of 1.2 percent in the growth rate of the number of firms.

- While the data show an important relationship between GSP growth and average tax rates, the impact of average tax rates on per capita income is less clear. A 1 percent increase in a state’s average tax rate can be expected to decrease per capita income by 0.07 percent.

- As previous studies have also noted, these findings can be sensitive to the time period, statistical methods, and variables used. Nevertheless, the results still lead to a general conclusion: not all tax variables exhibit a significant correlation with the selected measures of economic activity, but when they do, the relationship is usually negative.

CONCLUSION

Higher state taxes generally reduce state economic growth, GSP, and even population. It is clear that people produce or consume less, or even move to a different state, in response to higher taxes. Not all types of tax increases can be expected to significantly harm economic outcomes, but higher taxes are generally correlated with lower standards of living.