To read the full version, with citations, click here for PDF …

Exorbitant retirement benefits are threatening the ability of Rhode Island and its municipalities to deliver essential government services and, in one of the most extreme cases in the nation, one of Rhode Island’s municipalities has been driven into bankruptcy because of an inability to resolve pension debt issues through negotiation.

A recent decision by Rhode Island Superior Court Justice Taft-Carter has called into question whether the state and its municipalities have the flexibility to unilaterally adjust pension benefits. Our Center believes that Rhode Island does have broad legal flexibility to adjust existing pension benefits in order to stave off bankruptcy or avoid dramatic reductions in essential services. This policy brief considers the legal background of that question and suggests proactive steps which the legislature can take in order to guide future courts as they consider the constitutionality of proposed reforms.

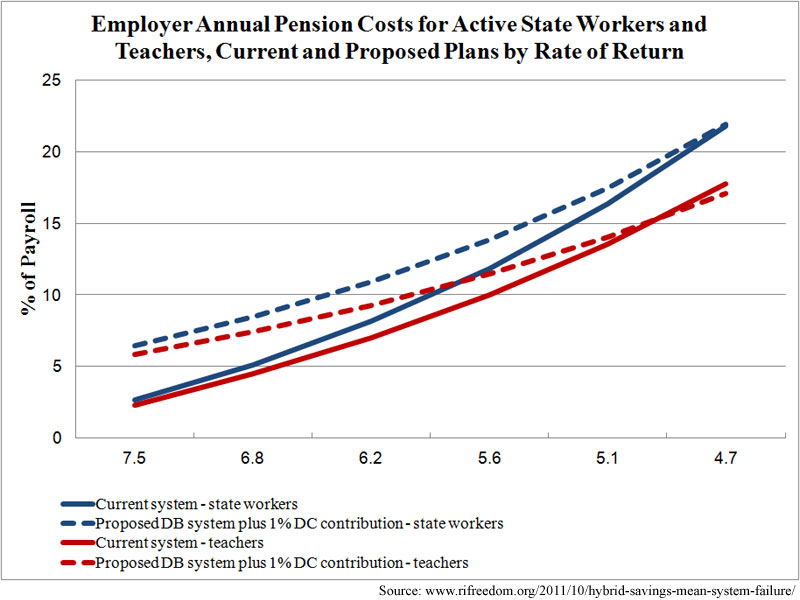

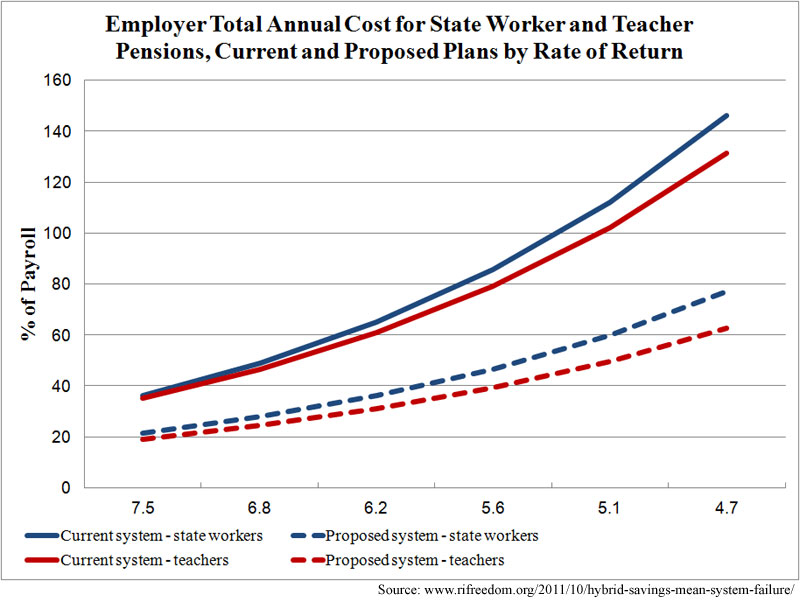

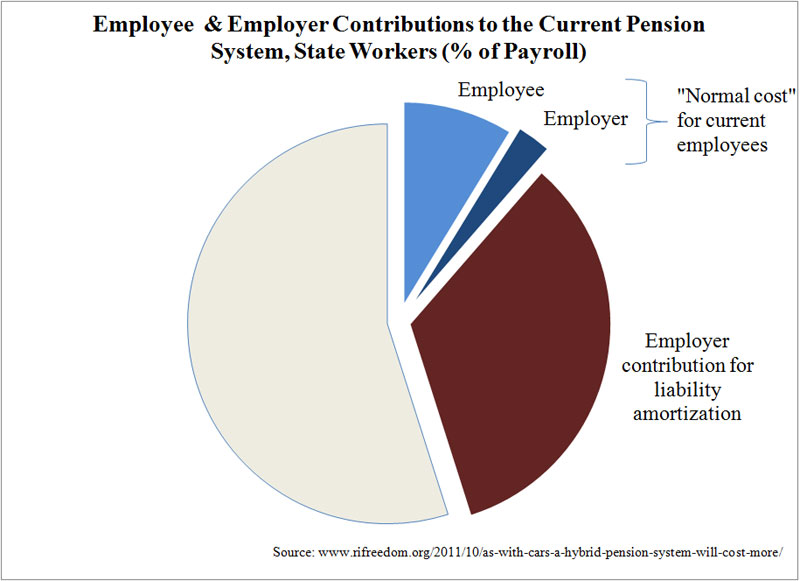

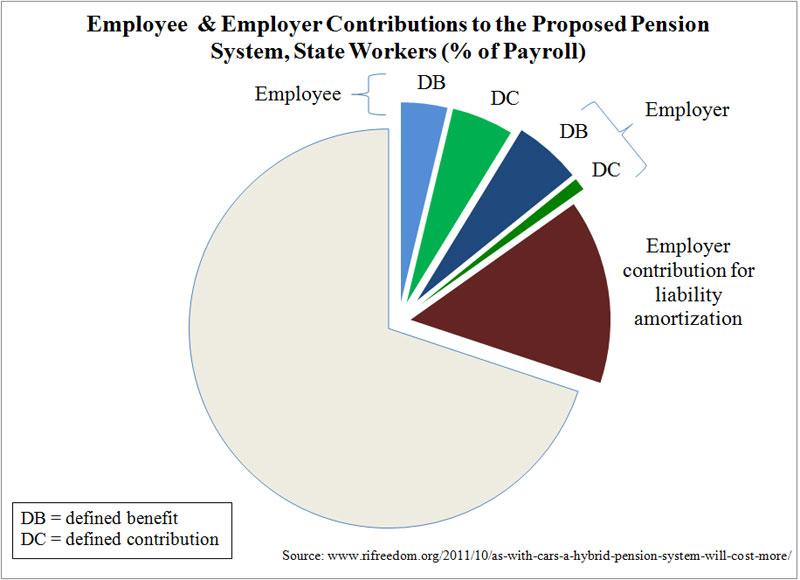

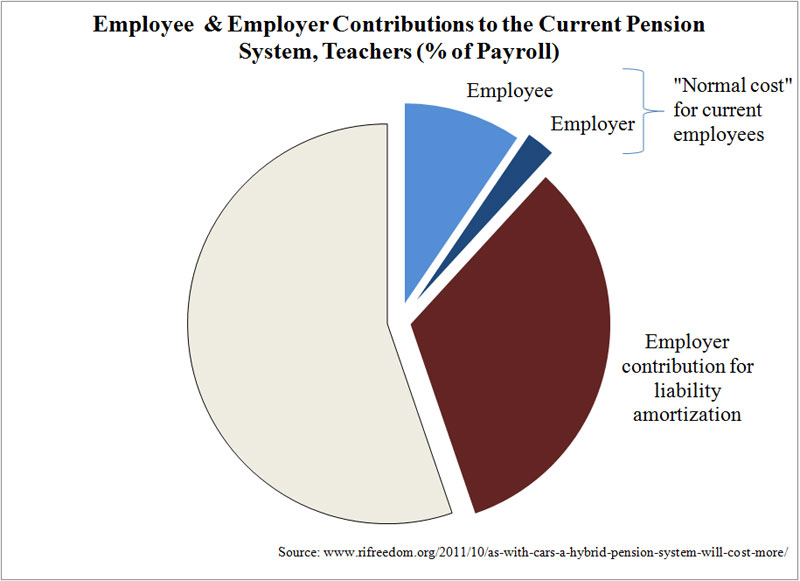

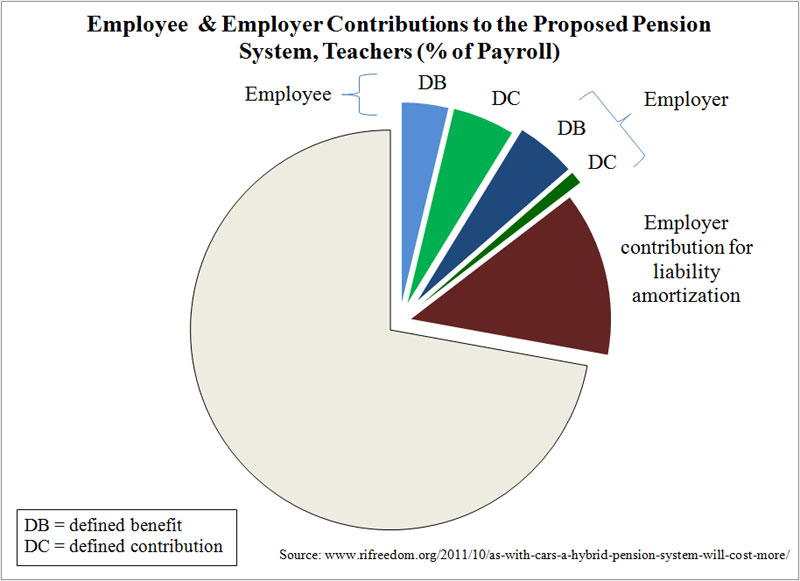

Most estimates place Rhode Island’s state level unfunded liability at approximately $6,800,000,000 ; a figure on scale with the state annual budget and roughly twice what the state collects in revenues in a year. Of great concern is that such estimates assume investment returns in the pension funds of 7.5 percent while many states are considering using estimates pegged to the money they pay for bond issues – potentially closer to 5 percent. If Rhode Island was to follow that more prudent approach, the unfunded liability would likely exceed twice the current estimates.

More importantly, a practical discount rate would more accurately reflect the expectations of beneficiaries as to the risk of their retirement plans. State and municipal retirees have long been led to believe that pensions were guaranteed by the government. In fact, pensions have always been some combination of promise and ‘gratuity,’ with payouts left to the discretion of politicians and future taxpayers.

And while a lower discount rate would expand the unfunded liability on paper, perhaps it is better to recognize that, for retirees, a conservative estimate of returns is more properly in line with their tolerance for risk.

Unfortunately, for current pensioners, those less conservative estimates of 7.5% returns or higher have been used for decades in Rhode Island and, while we can take the more prudent approach going forward, we must accept that for current participants in our retirement system, the money they were promised is simply not there.

Like the state, municipalities suffer under the burdens of their own liabilities and, with well over one-hundred separate plans, Rhode Island fails to realize savings related to economies of scale and more experienced oversight: Already some of our pensioners are suffering the consequences.

With the City of Central Falls in bankruptcy, its retirees are facing potential cuts to their pension checks of more than half what they had been receiving; a dramatic reduction to a fixed income that many cannot reasonably expect to afford. Poor planning, non-existent oversight, and bad political choices will, in a very real sense, be driving some of these pensioners into poverty.

As the Wall Street Journal’s David Wessel says, “Bankruptcy is a last resort. To avoid it, state and local governments need an alternative that is less unappealing. They don’t have one yet.” With 38 other cities and towns in Rhode Island facing the impacts of the same crisis, Governor Chafee recently called for alternate suggestions to the futility of trying to tax our way out of this deep hole.

There is growing bi-partisan recognition that exorbitant retirement benefits granted to civil service unions are threatening the ability of states and cities to provide essential services without implementing job-destroying tax increases. Indeed, even former San Francisco Mayor and California State Assembly Speaker Willie Brown (D), a staunch public union supporter, recognizes that lucrative defined benefit pension plans are unsustainable. John Fund of the Wall Street Journal writes about a column Willie Brown authored for the San Francisco Chronicle in which Brown lamented that civil service was out of control.

“The deal used to be that civil servants were paid less than private sector workers in exchange for an understanding that they had job security for life. But we politicians – pushed by our friends in labor – gradually expanded pay and benefits … while keeping the job protections and layering on incredibly generous retirement packages.”

Brown later told Fund, “When I was Speaker I was in charge of passing spending. When I became mayor I was in charge of paying for that spending. It was a wake-up call.”

Fortunately, despite the concerns raised by a recent Rhode Island Superior Court decision in the matter of Council 94 v. Carcieri , a more appealing remedy than bankruptcy exists. It is contained in two U.S. Supreme Court cases, Energy Reserves Group v. Kansas Power & Light and United States Trust Company of New York v. New Jersey .

States and (with state authority) municipalities, can unilaterally reduce excess retirement benefits under circumstances now widely prevailing. There is a widespread misunderstanding in many states that the U.S. Constitution prohibits these adjustments but there is no such prohibition. The Council 94 v. Carcieri decision has been misinterpreted as suggesting that Rhode Island has some unique version of that prohibition but that is not what the decision says.

In short, the Council 94 v. Carcieri decision simply states that some Rhode Island pensioners have certain contract rights. That is far from saying that those contract rights cannot be revoked when the state faces a pressing need.

A report published earlier this year by The Pew Center on the States confirmed that legislators’ belief that retirement benefits cannot be modified is only an assumption. “It is uncertain in many states what the constitutional protections are because they haven’t been tested or at least thoroughly tested in the courts,” says Ron Snell, director of state services at the National Conference of State Legislatures. “But state legislators have assumed the protections to be quite strong.”

This assumption that there is constitutional prohibition against benefit modification is a misunderstanding. Case precedent is clear that, under circumstances currently prevailing in many places, retirement benefits may be reduced. The U.S. Supreme Court’s interpretation of the U.S. Constitution lays out the rules by which states may modify their contractual obligations.

The facts required by the clear language of the governing cases are directly applicable to the situation in RI. These cases give us clear guidance.

There are scores of state and lower federal court cases holding against attempts to modify vested pension benefits. Upon examination, few, if any, of these cases were brought on the grounds set forth as applicable by the U.S. Supreme Court. Accordingly, these state and lower court cases are irrelevant to the current circumstances. They were special, very narrow cases that did not spring from legislative action to remedy a broad and general social or economic problem. The governing law may be summarized as follows:

• A state may impair a contractual right if it has a significant and legitimate public purpose such as remedying a broad and general social or economic problem, such as elimination of unforeseen windfall profits.

• A state may do so as an exercise of its police power.

• A contractual impairment may be constitutional if it is reasonable and necessary to serve an important public purpose.

When a state reduces an obligation, the courts will inquire as to whether the adjustment of “the rights and responsibilities of contracting parties is based upon reasonable conditions and is of a character appropriate to the public purpose justifying the legislation’s adoption. Courts properly defer to legislative judgment as to the necessity and reasonableness of a particular measure.”

When a state impairs its own contractual obligations (as is the case with retirement benefits promises) the courts and certain other material factors come into play. The courts will hold the state to a somewhat higher standard of scrutiny as to the policy’s necessity and reasonableness. Therefore, a prospering state with a well-funded retirement plan could not arbitrarily cut promised benefits. But a state struggling to the point of eliminating essential services or a municipality facing insolvency certainly may, under the law, modify existing retirement benefits. Furthermore, it is entirely settled law that one legislature may not abridge the powers of a succeeding legislature and cannot bargain away the police power of a state.

So, in addition to the realistic reading of the contracts clause itself, and as recognized by the Supreme Court, an independent doctrine holds that the Constitution’s contract clause does not require a state to adhere to a contract that surrenders an essential attribute of sovereignty. The classic doctrine that one legislature can neither abridge the powers of a succeeding legislature nor bargain away its police power permits states to reduce their public employee pension obligations under the circumstances now besetting many states.

The law does not permit a state to impair its contractual obligations arbitrarily or with impunity. The courts will look into whether a proposed impairment is reasonable and necessary to “serve an important public purpose”. Modifying existing pension benefits because the cost of providing them threatens a state or municipality’s ability to provide essential services or precipitating insolvency certainly rises to the standard of “remedying a broad and general social or economic problem.”

According to several well accepted doctrines and the clear holdings of the United States Supreme Court, if a state or, with a state’s authority, a municipality finds itself confronting a severe fiscal challenge based on exorbitant retirement pension obligations it is well within its inherent police powers to reduce its obligations to a reasonable level.

The courts will not rubber-stamp an arbitrary decision. Yet it is difficult to imagine a court finding that a reduction of such benefits to private sector levels for retirees of comparable circumstances to be ‘unreasonable,’ especially when the cost of providing those benefits threatens the ability to provide essential services.

Current evidence of reasonableness and necessity of such reductions includes:

1. extensive studies by respected nonpartisan institutes;

2. reports from respected media sources from across the political spectrum;

3. critiques by elected officials nationwide, both liberal and conservative, Democrat and Republican, of unjustifiably extravagant retirement benefits;

4. the documented growing inability of states and municipalities burdened by the cost of these retirement benefits to provide essential government services or maintain solvency.

Taken together, these factors are highly persuasive that it is reasonable and necessary to adjust certain states’ and municipalities’ pension obligations to the median level of private sector comparable positions. The power to unilaterally, though reasonably, reduce benefits provides a great deal more latitude for officials than many knew they had.

By taking this power into account, the Governor, the Treasurer, and the Rhode Island legislators who are considering solutions for addressing our pension crisis will find themselves positioned with many new options that they may not have realized were available.

Recognizing that, public officials simply may choose to reduce benefits of public workers to demonstrably reasonable levels. A good faith demonstration is all a state needs to reduce retirement benefits. This is simply done by showing they are implementing a remedy to a general economic problem and that such reductions are necessary and reasonable.

One approach, and one that has the added benefit of giving future courts a well-defined outline of legislative intent, would be to introduce and pass legislation laying out clearly and without hesitation the dramatic economic crisis now faced by the state. Such an Act would describe the need to assess the liabilities of the state and municipal pension funds with reference to rates of return reasonably in line with pensioners’ expectations of risk, would describe the limitation on additional sources of revenue to find the massive deficit, and would reference the dramatic reductions in essential services that are unavoidable if we fail to address the unfunded pension liability.

Therefore, the Rhode Island Center for Freedom and Prosperity recommends that the Rhode Island legislature acknowledge, through amendments to the laws governing Rhode Island’s state and local pension systems, that:

a. Pension benefits are promises limited by the ability of the system to pay, and are not binding contracts with pensioners;

b. A reasonable rate of return for pension investments should be equivalent to that of high-quality corporate bonds, as this is more in line with pensioner’s expectations as to the security of their retirement funds;

c. The unfunded liability of the state should be calculated using these more conservative rates and should be reduced to zero over a clearly defined period of time by modifications to existing pension plans that fairly reflect the economic circumstances we face as a state today and the detrimental impact on essential state services that this liability creates.

We further recommend that an extensive public record of such findings be established and preserved in order to leave no questions as to legislative intent and the factual basis for any proposed reforms. By taking this added step the executive branch and the general assembly will have made the job of the courts in ratifying such reforms all the easier, hopefully avoiding further costly legal battles, and providing pensioners with the clarity and predictability that they deserve.

***

About The Author

Giovanni D. Cicione Esq. is the Senor Policy Advisor to the Rhode Island Center for Freedom and Prosperity, a non-partisan and non-profit public policy group that advocates for free enterprise solutions to societal problems and for the protection of personal freedom. He received his Juris Doctor from Boston University Law School, a bachelors degree in Philosophy from George Mason University, and is a member of the Bar of the State of Rhode Island and of the Commonwealth of Massachusetts.

***

To read the full version, with citations, click here for PDF …