Hybrid Savings Mean System Failure

The only argument that I’ve heard against my suggestion that the proposed hybrid pension system will be more expensive than the current system is that the hybrid offloads market risk onto the employee, alleviating the risk to the employer (i.e., us, the taxpayers). Moderate Party founder and gubernatorial candidate Ken Block made the point on Anchor Rising, and Gary Morse, pension adviser to the Republican who was almost governor, John Robitaille, called in when I was on Friday’s Dan Yorke Show to make a similar point.

My response has been to suggest that, while the objection may be true, the entire pension reform relies on the 7.5% rate of return that the state’s actuaries have assumed. As a reminder, the current system is a defined benefit plan, which promises employees a certain retirement package; the hybrid system would decrease that benefit but put money into a 401(k)-style plan for each employee to fill in the gap. Right now, the major problem is the liability for defined benefit promises already made, and the hybrid doesn’t make those go away.

Unfortunately, I haven’t come across “what if” data from the actuaries that allows a real comparison of the system’s health with different rates of investment return. One can, however, infer the effect of the Retirement Board’s recent lowering of the return rate assumption from 8.25% to 7.5% from the latest actuarial report. Specifically, the Board dropped the rate of return by 9%, and the normal cost of an active employee’s pension (that is, the percentage of payroll that must be put aside to fund an individual employee’s retirement) went up by 22% for state workers and 18% for teachers.

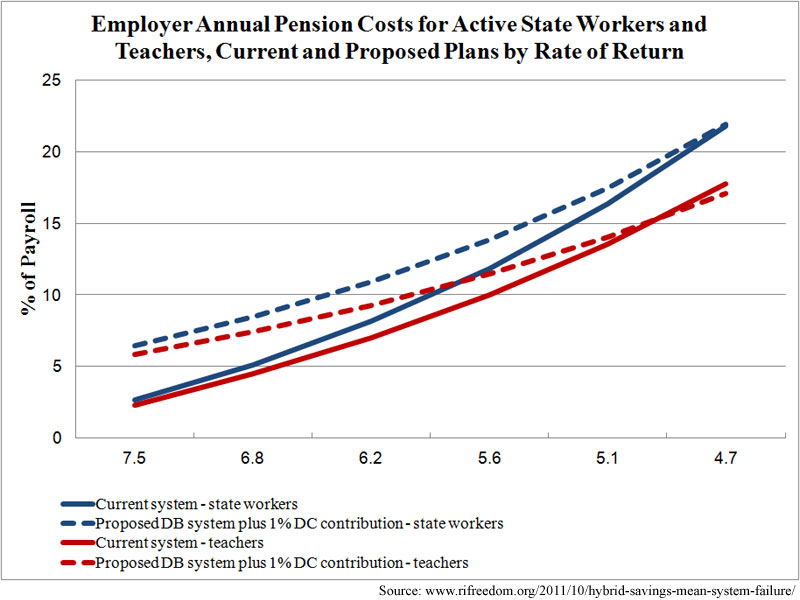

For an accurate “what if” scenario, the actuaries would have to apply the different assumptions to their models, but purely for the sake of illustrating my point about the cost of the hybrid plan, I’ve assumed that same return-rate-to-normal-cost ratio applies consistently to the equation. If that’s accurate, then the hybrid plan doesn’t cost the taxpayer less than the current system unless the market returns less than 5% on investment:

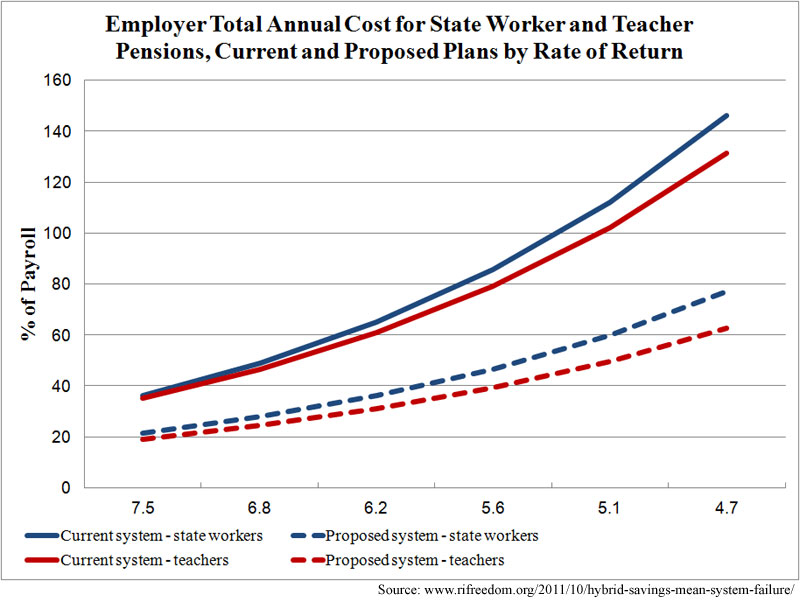

The solid lines show the effects of an under-performing market on the current defined-benefit plan; the dotted lines show its effects on the hybrid plan. And, yes, the lines do cross eventually. However, under those circumstances, the total cost for the pension system to the employer, even under the reform, will be well above the annual cost that currently has everybody in a panic — over 60% of payroll for teachers and nearing 80% of payroll for state workers:

Of course, the solid lines, which track the current system, show just how scary the situation will be if the General Assembly does nothing, and a defined contribution component ought to be part of the solution (if not all of it). That doesn’t mean, though, that reformers should take the system on the table just because it incorporates some worthwhile concepts. If this reform passes, it’ll be years before the panic level rises sufficiently for further action by elected officials, and by that point hundreds of millions of dollars will have been siphoned into untouchable defined-contribution accounts.

Leave a Reply

Want to join the discussion?Feel free to contribute!