January 23, 2014

TO: Joint Sales Tax Study Commission #6

FROM: Mike Stenhouse, CEO

SUBJECT: Prepared Testimony Remarks

Good evening. I’d like to first thank the Commission members for their hard work and open minds when it comes to creating jobs and renewed opportunities for Rhode Island families via a new growth economy.

Today, Chairman Malik asked this Commission to consider how to manage the budget implications of potential sales tax reform in Rhode Island. So today, we’re going to talk about revenues and spending. However in light of the earlier, it may be appropriate to review why we’re here.

In fact, perhaps the Governor framed the debate best by suggesting in his recent State of the State address, in effect, that government should play an aggressive role in shaping people’s lives. As we discussed at the last hearing, our sales tax issue all boils down to a larger, philosophical approach as to the proper level of government intervention in our personal lives and in the conduct our business. Indeed, this sales tax issue in Rhode Island has evolved to become part of a larger national debate about “income inequality”.

If we as a state believe that the status quo is hunky-dory for our state, and that generous government services that incentivize people to live a life of dependence is good, then yes, you’ll be inclined to think that more of the same philosophies, policies, and modeling tools utilized, to fall to where we are now, should be what we continue to utilize in the future. The state’s REMI tool falls in this category.

If you believe like we do, that the status quo is the enemy of our future, that every person should have the opportunity to become self-sufficient and thrive, then you’ll be inclined to look for a new approach, and new solutions. Our Center’s RI-STAMP tool represents that new way of thinking.

The old way or a new way? … that is the question. Preserving the current system, or helping our state’s residents?

The testimony you just heard regarding the state’s tax modeling tool, REMI, should not cause you to take your eye off the ball. The question at hand is not which modeling tool is better; rather, the critical question is whether or not the state’s recent economic troubles and its own modeling tool are credible enough reasons to dissuade you from considering the bold NEW reform our Center is recommending and that virtually every witness you heard from supports.

It should be clear to everyone that what we’re doing now – the old way – is NOT working. And virtually everybody outside of the system understands that. The handout we provided to you summarizes the testimony you heard from our prior six hearings. For those of you watching at home, this handout can be viewed on our website – RIFreedom.org – I believe it’s the second item down, called “Testimony Highlights.”

We all heard overwhelming testimony in support of reform from dozens of real residents and real business owners. The only pushback you’ve heard, are from those connected with the system. Again I ask, is good government about preserving the system or helping people?

Taking a step back. Over the past year, as our Center has been raising awareness about the many benefits of repealing the sales tax, I have, admittedly been astounded by the lack of concern about how those benefits might improve the lives of real people. The first reaction, and the disqualifying consideration, right off the bat, for many, is … well how do we make up all the revenues? To the political class – “revenues” are more important than creating opportunities for our fellow Ocean Staters. Our Centers believes otherwise … do you?

When it comes to the impact on the state’s budget regarding sales tax reform, or any tax reform for that matter, I am here to proffer that current levels of spending are hurting our state. To move forward with major tax reform, we must first accept that “revenue-neutral” policies – or limiting ourselves to simply reshuffling the chairs on the deck – are not likely to produce anywhere near the desired economic and jobs boost our state so clearly needs. If, after years of increasing revenues and spending – via taxation – to levels that have caused wreckage to our economy … if, we want to reverse course and actually do something productive that creates economic growth, then it only makes sense that we also must reverse course when it comes to levels of government spending.

If we want economic growth and more shoppers and businesses in this state … as you heard from witness after witness before this very Commission… we must have lower levels taxation, and give them a reason to come to RI. To lower tax levels to be attractive in this regard, we must necessarily lower levels of state spending. We can do this. It is in within the power of this Commission to recommend this. It is in the power of the General Assembly to implement your recommendations … it is allowed!

Across the nation in 2013, economic growth became a top priority for dozens of states; in fact, in 2013, 18 states actually cut taxes! They were allowed to … and they did. In Wisconsin, Governor Walker has proposed $800 million in tax cuts.

A few years ago, Rhode Island, along with Michigan and Indiana, was among the three worst states, nationally, when it came to recovering total jobs, as compared with pre-recession levels. Two states decided to take bold action to change that bold dynamic … yet one state did virtually nothing. Want to guess what state that was? Michigan and Indiana became Right To Work states. Separately, even a perennial high tax state such as NY is now actively promoting tax-free zones to attract and expand businesses. Rhode Island’s opportunity to remain competitive, in its own way, is significant sales tax reform. Will we do it?

Yet there are many for whom the preservation of the size government spending is a more important consideration. Indeed, it is the overall mission of our Center to provide a very different perspective, to think outside that box, and to inject new ideas into the public policy debate, to challenge that status quo thinking.

However, those who defend the status quo see our Center as being disruptive to a political process that has an insatiable appetite for more of our money. We believe a healthy democracy necessarily means rigorous debate. If our Center’s advocacy is seen as disruptive, then so be it … we just see it as a debate. We believe our state needs a new public policy culture. But the status quo is firmly entrenched in our state.

And so far in 2014, we have heard nothing but the same old ‘reshuffling of the chairs on the deck’ from our political leaders.

And what is the status quo that they’re defending? Revenues – on a piece of paper. It seems it’s always about spending. Instead of looking to enhance the well-being of Ocean Staters, our government looks at us as nothing more than ATM machines … to serve the government’s priorities. It is this policy culture that must be changed. It is allowed, and today, you have the power to suggest a bold new step for our state.

Rhode Island is not defined by the amount of money that can be extracted from its residents and businesses, nor by a number at the bottom of a spreadsheet. Rhode Island is not about the size of its government. Rhode Island is about the hopes and dreams of its people – real families who are looking improve their futures through increased opportunities for prosperity.

The status quo that we oppose is all about preserving the system. The reforms we advocate for are about real people –and job opportunities – and about preserving Rhode Island as home to more and more families and businesses.

You may recall that in my first testimony to this committee in September that I showed you a few charts to keep in mind. Allow me to review:

- This first chart is what the status quo system is about … ever increasing levels of spending, 25% higher than what inflation and our meager population growth would otherwise dictate.

- This next chart depicts just one part of the unintended consequence of that approach – showing Rhode Islanders flocking out of our state to neighboring counties in MA and CT to escape to lower tax burden states. Not because of weather.

- An this final image portrays the real-life effect … fewer and fewer people at grandma’s dinner table.

A report in today’s ProJo showed that the Census Bureau determined that another 3,922 Rhode Islanders moved out of our state last year. Cutting the oppressive levels of state spending and taxation that caused this undesirable out-migration is possible. We are allowed to do it.

(NOTE: at this point, the testimony was interrupted and not allowed to be completed in its entirety. Only the non-italicized content below was later spoken to the Commission)

Our Zero.Zero report and recommendation is clearly a departure from the current way of thinking. We intended it to serve that very purpose. And we used a tool, STAMP, that offers a different perspective on how to impact a state’s economy – has the current perspective worked?

I’d like to repeat what I said at the last hearing: RI is the #1 state in the country when it comes to government spending in the form of “income redistribution”. In theory, if government spending is indeed a stimulus to a state’s economy, and if RI has been doing this at a higher level than most other states, then it would stand to reason that RI should have one of the nation’s best economies.

Sadly, however, Rhode Island’s reality clearly suggests that this formula of high spending has not worked for our state. As Commission members, it’s up to you to decide whether or not continuing with this same approach will work best for our state’s future. Or whether a new course is warranted.

It is the position of our Center that instead of making “government revenues” as the state’s number one priority, that we should consider the well-being and future of the taxpayers and residents of our state as paramount! How can we possibly justify limiting their dreams of a brighter future, solely in order to expand the system and the amount of money the state collects and spends?

Let me share with you a vision we have that that new approach might create. Instead of the seeing the tail-lights of our loved one who are leaving our state, imagine the headlights of cars on I-95 jammed with the traffic of family members, entrepreneurs, investors, and shoppers streaming over the border into Rhode Island. Imagine the parking lots of RI retailers splattered with cars with MA or CT license plates, and, of the extra workers those retailers are able to hire.

This is what our Center’s sales tax recommendations are all about, as well as putting money back in the pockets of every single individual and business in the state, and for creating thousands of new jobs so that they can have new opportunities and mobility to move up the income ladder and improve their lives.

In December, a new study showed that while homelessness is decreasing nationally, it has actually increased in Rhode Island. Clearly, increased levels of spending have not worked for those families and individuals in our state.

Our unemployment rate, though better overall, is not keeping pace with our New England neighbors or the rest of the nation? In fact, we are dead last. Is this acceptable? Is this government working for us?

In fact, even State Tax Administrator, David M. Sullivan, said in November in the ProJo that the recent liquor/wine tax cuts should help to spur sales and boost the state’s economy at an important time for retailers. Why would this effect not be the same across all industries if RI were to obtain a competitive sales tax advantage via its repeal?

So I ask: What should we be more concerned about: keeping firmly to arbitrary government spending levels? Or providing real opportunities for families in need and putting them back at real family dining tables?

If we want out-of-the-box solutions, then we must not box ourselves in by considering only revenue-neutral options.

The future of Rhode Island families can no longer be held hostage by a bloated state budget. You heard testimony from a national tax expert who said that RI simply does not have the tax base to try to pay for all the services currently on our books. Yet we keep trying to serve more people and spending more and more.

We believe that our state has been doing it precisely backwards. We have to grow our state’s tax base, by creating an environment where more people will choose to make RI their home, not further burden those who remain.

In our view, the state budget should be reflective of the goals and aspirations we set for ourselves as proud and aspiring Rhode Islanders … it should not serve to limit those dreams. Our spending priorities must be aligned with advancing our overall well-being … not advancing government to our overall detriment … government spending must be “right-sized”.

So I ask you to again consider the critical question … the old way or a new way? Should this Commission be dissuaded from supporting potential game-changing policy reforms, such as repealing the sales tax, simply because it’s different from our current failed approach? Or because it is not a revenue-neutral solution?

In the end, it is up to you to recommend which course will best work for Rhode Island. It’s time to dare to buck the system and forge a new future for our state. It is allowed.

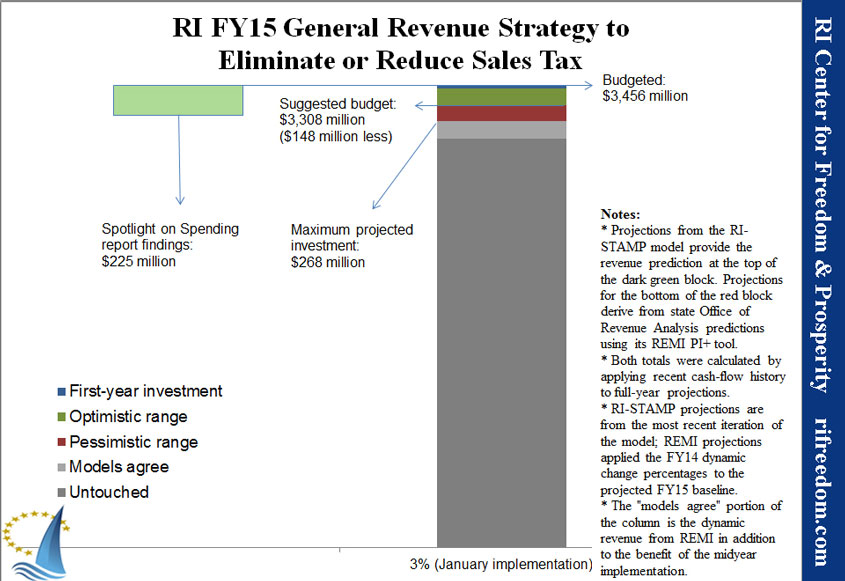

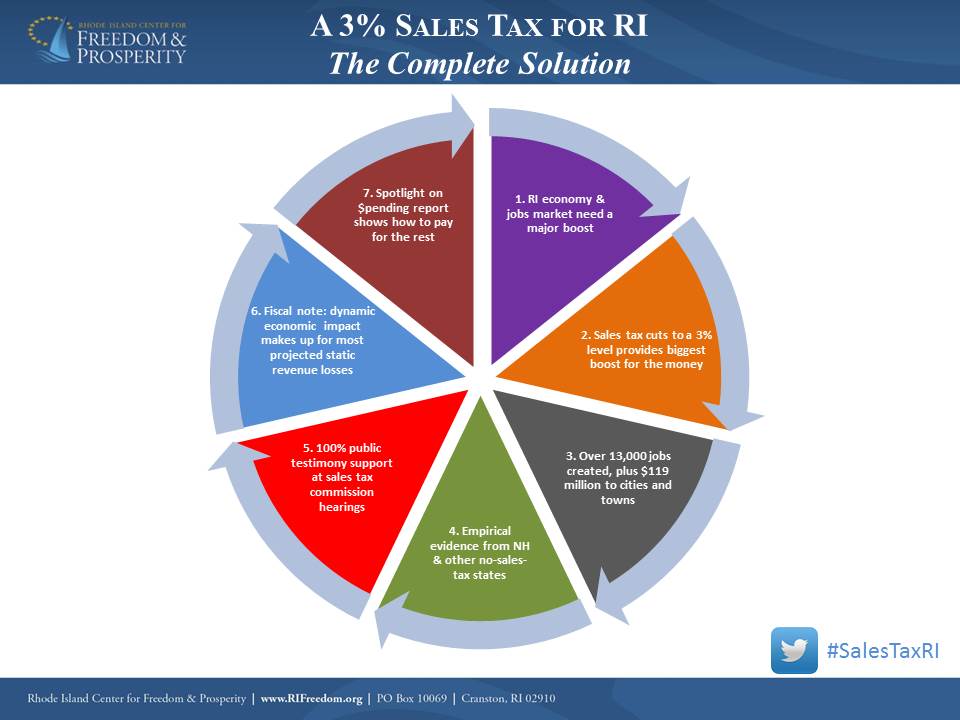

With regard to specific recommendations from this Commission, our Center hopes that you will decide to take the boldest action by repealing the sales tax entirely, down to Zero.Zero %, and creating the most jobs. Note that we propose to implement this reform as of October 1, so as to spread out the budget impact over two years, and realize one quarter of sales tax revenues in the next fiscal year.

Think of the low-income families who will keep more of their money in their own pockets and who might find new job opportunities because of the new growth economy.

Think of the small business owners and restaurants who will no longer have to struggle to comply with the unfunded mandate that they collect taxes on behalf of the state, or spend thousands of dollars in time an legal fees when trying to settle a dispute with the state.

Think of the cities and towns that will collectively realize over $100 million in new commercial property tax revenues.

And, for those of you who will participate in this election year, think of how voters will reward you when you support an initiative that will save money for every single family and business in the state.

Something I neglected to mention last hearing and that I ask you to keep in mind, is that any sales tax reduction plan – that does not bring the rate all the way to 0.0% – does little, if anything, to lessen the business compliance costs of this unfunded mandate on retailers, restaurants, and other businesses that have a retail sales permit. Nor can any budget savings be realized through a reduction in the size of the government apparatus designed to audit and collect sales tax revenues.

Any sales tax rate above 0.0% would likely require just as much government infrastructure and just as many compliance burdens for businesses as the current 7% rate.

A recent report cited Rhode Island as being out of compliance with its tax collection on the recently enacted sales tax on high-end clothing. Repealing the sales tax entirely eliminates these unnecessary complexities and costs of collection, and also puts all RI industries on a level playing field, and will end future nonsensical debates about which industries to tax and which to leave alone.

Our Center additionally suggests two other related recommendations be considered by this commission: first, that a comprehensive review of existing penalties and interest on back sales tax owed be conducted to determine if those statutes are making it overly difficult for businesses to remain open; second, that with sales tax reform that adjustments be made to the current 4% tax levy cap on cities towns so as to allow them to realize the organic revenue growth they will see from a lowered sales tax.

For the first time in decades, our state has the opportunity to take a major step in a new public policy direction, and send a signal to Rhode Islanders that their government places their well-being as top priority.

In Rhode Island in 2014, this Sales Tax Repeal Study Commission represents the only hope to take to take a major step in a new direction. Rhode Island needs to keep pace with other states. Repealing or rolling-back the sales tax appears to be the only significant economic development policy idea on the table for the entire 2014 legislative session …not only is this something we are allowed to do, but that we must do

The budget can be amended to allow for this, if we have the foresight and take the proper steps to plan how to do it. In this regard, I’d like to introduce our Center’s research director, Justin Katz, who will take you through some of the budget considerations in our original report. Justin will also suggest revenue and spending guidelines that may be helpful to you in determining how the budget may be flexibly managed if significant sales tax reforms are implemented. Thank you.