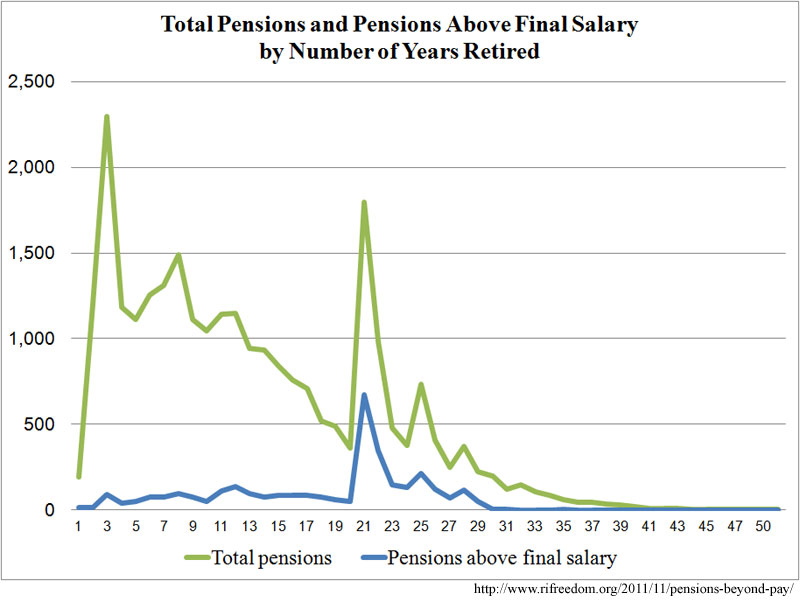

The Significance of Small Pensions

In the public debate about suspending cost of living adjustments (COLAs) for retirees holding public-sector pensions, the most compelling argument addresses retirees whose income would drift below the poverty level as inflation erodes their pensions’ value. It’s important to adjust one’s reaction, however, to account for the variation in individual circumstances. One cannot assume, that is, that each pension is the sole source of income (even sole pension) for the retiree.

Take the pensioners in the Municipal Employees Retirement System (MERS), which the state administers and which has the lowest average gross pension (including COLAs) among the state’s various plans. According to data available on RIOpenGov.org, the average for the 3,972 pensions in the municipal system is $13,285 per year. Of those, 59 pensions are worth less than $1,000 per year — clearly not sufficient as a sole source of income; that’s 1.5% of MERS pensions, and it reduces the average by $192.

Expanding the range to include all pensions under $5,000 — still not enough to be more than supplemental income — brings the total to 799 pensions. Excluding them from the equation — on the grounds that we’re interested in the plight of retirees who live on their pensions alone and therefore cannot be made to suffer COLA suspensions — brings the average MERS pension up to $15,842, which is 45% greater than current poverty guidelines for an individual.

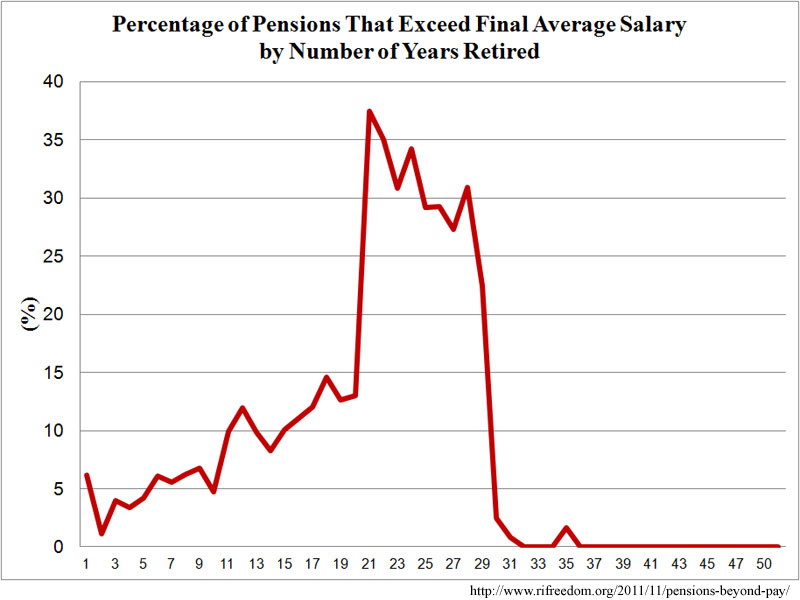

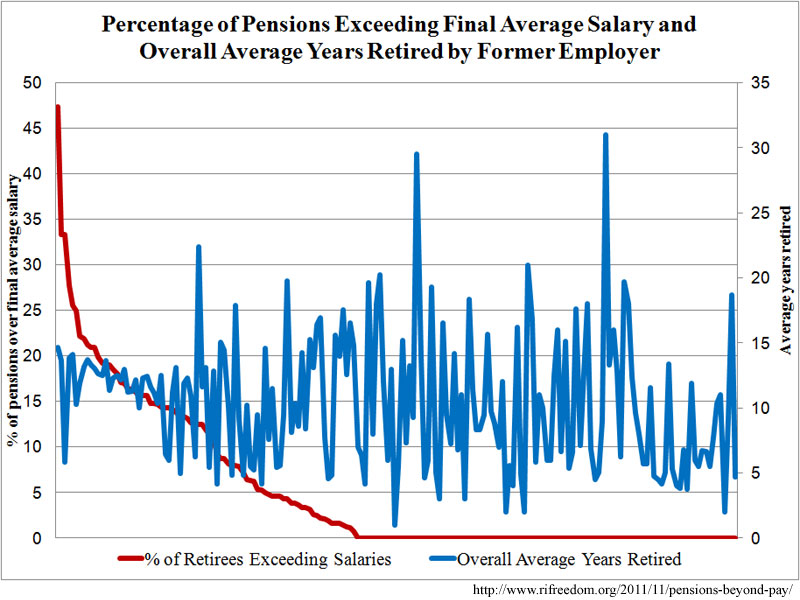

That still isn’t a great deal of money, but the relevant point is that many of these pensions are so small that it isn’t reasonable to present them as the retiree’s livelihood. Among all retirees, the average gross pension is approximately 71% of the final average salary that the person earned while working. That means that a pension of $5,000 would result from an employee’s pay of $7,000; such employees surely had other resources while working and may very well in retirement, too.

Unfortunately, payroll information for public employees has only been readily available to the public for a few years; it often isn’t descriptive of the working capacity of the employee; and very few retirees with low pensions retired recently. That last point, in itself, is very interesting: Among all 26,598 retirees, the average date of retirement is July 1998. For those with pensions under $10,000, it’s August 1994; under $5,000, January 1992; and under $1,000, October 1994. In general, and despite COLAs, those with the smallest pensions have been retired for longer. It would require extensive research to confirm, but the impression given is of the bad old days when pensions were easy rewards to give for minimal service.

Double/Triple Dipping

In some cases, the additional income for retirees derives from additional pensions. Of the 26,598 pensions on the state’s books, 1,195, or 4.5%, go to former employees who have more than one, and the average combined pension for these 574 individuals is $48,911. Five hundred and twenty nine have two pensions; forty-five have three.

(Identity was determined by full name, including middle initial or lack thereof, year of birth, and current city of residence. Also note that these totals include individuals who also receive “teacher survivor benefits” as a pension in lieu of similar provisions in Social Security, as well as retirees who receive pensions as “beneficiaries” but are not the original “owners” of them.)

In the interest of privacy, it’s preferable to discuss pensions in aggregate terms, but in this particular case, it’s impossible to convey a sense of things without pointing to at least a few specific examples. For that purpose, here are the twenty highest-paid retirees whose totals involve more than one pension:

| Top 20 Retirees with Multiple Pensions, 2010 |

|

Age at Retirement |

Former Employer |

Year of Retirement |

Gross Pension 2010 ($) |

Carmine DiPetrillo

$164,795 |

67

|

Legislators (O) |

1994

|

12,252

|

|

67

|

State Police Judge – Family Court (O) |

1994

|

152,543

|

Peter O’Connell

$134,907 |

69

|

State Police Judge (O) |

1990

|

92,776

|

|

72

|

State (O) |

1993

|

42,131

|

Deborah Jones

$130,926 |

50

|

Cumberland School Dept. (B) |

2002

|

40,083

|

|

50

|

TSB |

2002

|

22,500

|

|

56

|

Cumberland School Dept. (O) |

2008

|

68,343

|

Elizabeth Vendituoli

$130,598 |

54

|

Bristol Warren Reg. School Dist. (B) |

2005

|

42,401

|

|

54

|

TSB |

2005

|

22,500

|

|

55

|

Bristol Warren Reg. School Dist. (O) |

2006

|

65,697

|

Mary McCabe

$127,781 |

43

|

State (B) |

1984

|

44,940

|

|

63

|

State (O) |

2004

|

82,841

|

Audrey Carnevale

$125,330 |

47

|

Legislators (B) |

2000

|

9,501

|

|

47

|

State (B) |

2000

|

68,498

|

|

52

|

State (O) |

2005

|

47,331

|

Robert Gerus

$124,520 |

60

|

Cumberland School Dept. (B) |

2003

|

35,989

|

|

60

|

TSB |

2003

|

17,930

|

|

61

|

State (O) |

2004

|

70,601

|

Clifford Cawley

$121,082 |

59

|

Legislators (O) |

1987

|

19,896

|

|

59

|

State Police Judge – Superior Court (O) |

1987

|

101,186

|

Vincent Cullen

$120,542 |

55

|

Cranston School Dept. (B) |

1989

|

4,667

|

|

55

|

TSB |

1989

|

16,137

|

|

68

|

State (O) |

2002

|

99,738

|

Samuel Greenstein

$120,246 |

57

|

Providence School Dept. (B) |

2002

|

42,527

|

|

57

|

Providence School Dept. (O) |

2002

|

77,719

|

Marcia Clifford

$118,956 |

38

|

State Police Judge (B) |

1987

|

56,229

|

|

52

|

State (O) |

2001

|

62,727

|

Susan Browning

$116,254 |

53

|

Providence School Dept. (O) |

2001

|

57,996

|

|

54

|

Coventry Public Schools (B) |

2002

|

42,388

|

|

54

|

TSB |

2002

|

15,870

|

Livia Giroux

$112,609 |

48

|

Smithfield School Dept. (B) |

1990

|

33,534

|

|

48

|

TSB |

1990

|

13,500

|

|

62

|

West Warwick School Dept. (O) |

2004

|

65,575

|

Francine Gonnella

$109,369 |

63

|

Judges – Superior Court (B) |

2007

|

34,666

|

|

63

|

Providence School Dept. (O) |

2007

|

74,703

|

Rita Munzer

$107,113 |

63

|

Warwick School Dept. (O) |

1983

|

29,936

|

|

66

|

State (B) |

1986

|

55,896

|

|

85

|

State (B) |

2005

|

21,281

|

Geraldine Guglielmino

$106,838 |

63

|

State (B) |

1998

|

39,156

|

|

64

|

State (O) |

1999

|

67,682

|

Sydney Williams

$106,371 |

58

|

Newport School Dept. (O) |

1986

|

64,752

|

|

63

|

Newport School Dept. (B) |

1991

|

23,689

|

|

76

|

TSB |

2004

|

17,930

|

Gladys Thomas

$105,769 |

53

|

State (B) |

1989

|

34,887

|

|

61

|

State (O) |

1997

|

70,882

|

Nancy Cunningham

$104,988 |

58

|

State (B) |

1989

|

69,074

|

|

59

|

North Kingstown School Dept. (O) |

1990

|

35,914

|

Marcella Delnero

$102,464 |

59

|

State Police Judge – District Court (B) |

1988

|

49,997

|

|

61

|

Newport School Dept. (O) |

1990

|

52,467

|

Notes:

“O” = owner

“B” = beneficiary

“TSB” = Teacher Survivor Benefit

Identity was determined by full name, including middle initial or lack thereof, year of birth, and current city of residence. |

The Individual Stories

Sifting through the pension list in order to understand the decisions behind the numbers is fascinating, but time consuming — not the least, as noted above, because the available data is sparse, recent, and incomplete.

For example, trying to figure out the lives and deals behind the very low pensions, one might come across John Marchant, who receives $609 per year based on work with the Town of Scituate. He appears to have “retired” in September 2007, so he shows up on a payroll filing from that town available on The Money Trail, showing his pay as $2,000, without description of his job. Another angle comes into view with Joseph F. Cassidy, who receives $333 annually for a non-teaching role in the Pawtucket School Dept., which he left in 1979. An Internet search for Mr. Cassidy turns up an RI House resolution from June 2010 congratulating his son upon his retirement as Director of Planning and Redevelopment for the City of Pawtucket. (The pension rolls are full of repeated last names.)

The double- and triple-dip pensions are even more intriguing but require some delicacy, because the better part of them appear to involve a deceased spouse. Deborah Jones, for instance, has been receiving a pension as a “beneficiary” and a TSB since 2002, totaling $62,583. She then retired from the same district, adding another pension in 2008. The payroll for her final year has her receiving $73,334 as a substitute teacher.

None of this should be taken as evidence of wrongdoing on the individuals’ part. Behind the pension statistics are people trying to make the best decisions that they can as they deal with the unpredictable events and opportunities of life. But as Rhode Island’s retirement system devolves into further crisis and state officials come forward with proposals to resolve (or at least postpone) it, honest assessment and tough judgment are the order of the day.

After all, behind the “employer contributions” are taxpayers struggling to get by in an atrophied economy while public decision makers treat retirements that are both long and lavish by private-sector standards as inviolable commitments.